If you’re thinking about retiring, it can be helpful to understand what your preservation age is and how it affects your ability to access your super.

What is preservation age?

Your preservation age is generally the earliest age you can access your super, and it’s calculated based on your date of birth. It’s called preservation age because your super is a preserved benefit – locked away until you reach a certain age. You can find out your preservation age below.

|

Date of birth |

Preservation age |

|

Before 1 July 1960 |

55 |

|

1 July 1960 – 30 June 1961 |

56 |

|

1 July 1961 – 30 June 1962 |

57 |

|

1 July 1962 – 30 June 1963 |

58 |

|

1 July 1963 – 30 June 1964 |

59 |

|

From 1 July 1964 |

60 |

Once you reach your preservation age and meet a condition of release such as retiring, you can start accessing the retirement savings you’ve been accumulating during your working life.

It’s worth noting preservation age is different from the Age Pension eligibility age, which also depends on your birthday. Age Pension. eligibility is currently set at 66.5 years but will change to 67 years on 1 July 2023. Find out more

Do I have to retire when I reach preservation age?

No. Your preservation age doesn’t need to be the age you retire unless you want it to be. If you’re willing and able, it’s possible to carry on working beyond your preservation age.

If you continue working, you can keep building up your super by making personal deductible contributions, or if you are an employee, this can also be achieved through employer contributions (using the Super Guarantee rate, if eligible), or salary sacrifice contributions.

What can I do once I reach preservation age?

If you’ve reached preservation age and meet a condition of release, you can access your super. Some options have restrictions on the amount of super you can access. Here are some common options:

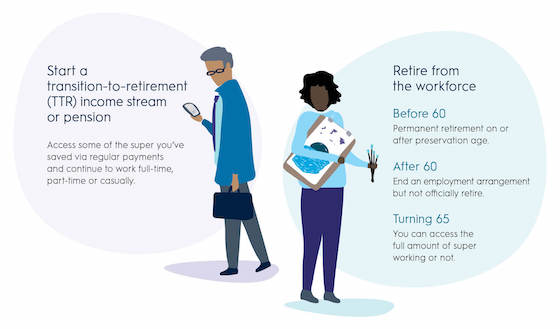

Starting a transition-to-retirement (TTR) income stream or pension

Under this condition you can access some of the super you’ve saved via regular payments once you reach your preservation age, while continuing to work full-time, part-time or casually.

Retiring from the workforce

Once you’ve met a retirement condition of release, there are no restrictions and you can access the full amount of your superannuation savings. The definition of retirement can be different depending on your age:

-

Retirement before age 60

Once you’ve reached your preservation age, and you’re permanently retired, you will be able to access your superannuation without restrictions. You’ll likely have to make a declaration to your super fund that you don’t have any plans to work (for an income) again.

-

Stopping an employment arrangement after you reach 60

From age 60, you can leave your job (but not officially retire), and don’t have to make any declaration about your future employment intentions. You can access your super and, if you wish to at some point, return to work. However, any earnings or contributions accrued after you leave your job can’t be accessed until a fresh condition of release is met.

-

Turning 65

Whether you’re still working or not, once you’ve reached 65, you can access the full amount of your super.

There are also some specific circumstances not related to retirement, such as financial hardship, where the law allows early access to your super, even if you haven’t reached preservation age.

What’s the best way to access my super?

This will depend on your circumstances, the kind of lifestyle you want and how long you’d ideally like your savings to last.

Drawing on your superannuation in the form of a pension is a common option. A pension is a series of regular payments made as a super income stream. There are different types of pensions to suit your needs and circumstances such as transition to retirement pensions or account-based pensions (also known as allocated pensions).

You can also choose to receive your super via an annuity, or as a lump sum. Find out more about the different types of retirement and superannuation pensions.

An account-based pension or annuity is a retirement income stream that pays out your super savings but will stop once your super savings are depleted, or if you convert your income stream to a lump sum.

It’s worth considering how withdrawing super can affect your tax, and any Centrelink payments (including the Age Pension).

Remember, your super is entirely separate to the Age Pension. Depending on your financial situation, you may be entitled to a full or part Age Pension from the government, or nothing at all.

Where can I get more help?

Doing your research and making a plan for your retirement can help ensure you’re making the most of the options available.

Source: AMP July 2021

Important:

This information is provided by AMP Life Limited. It is general information only and hasn’t taken your circumstances into account. It’s important to consider your particular circumstances and the relevant Product Disclosure Statement or Terms and Conditions, available by calling 02 6947 2866, before deciding what’s right for you.

All information in this article is subject to change without notice. Although the information is from sources considered reliable, AMP and our company do not guarantee that it is accurate or complete. You should not rely upon it and should seek professional advice before making any financial decision. Except where liability under any statute cannot be excluded, AMP and our company do not accept any liability for any resulting loss or damage of the reader or any other person. Any links have been provided for information purposes only and will take you to external websites. Note: Our company does not endorse and is not responsible for the accuracy of the contents/information contained within the linked site(s) accessible from this page.